Personal circumstances

A safe choice for every situation in life

The Pension Fund is a key component of your personal financial planning and can have a significant impact on your financial security in retirement. Find out everything you need to know about different circumstances in life: from joining our Pension Fund and buying your own home all the way to retirement.

Admission to the Pension Fund

Members join the Hitachi Group Pension Fund on commencement of their employment contract, at the earliest on the following dates:

- Age 18: Admission to the Pension Fund for insurance of the risks of disability and death.

- Age 21: Admission to the Pension Fund for retirement insurance.

Buy-in

Buy-ins are voluntary contributions made by members to the pension fund. The conditions governing buy-ins – in particular the maximum amount – are specified in the rules.

In the event of death, the total personal buy-ins into the pension fund, less any early withdrawals for home ownership or divorce payments, will be disbursed to the eligible beneficiaries.

Tax implications must be taken into account. Members are solely responsible for the tax effects of their buy-ins and any lump-sum withdrawals. The Hitachi Group Pension does not assume any liability for objections raised by the tax authorities.

Death

The HR office reports the death of a member to the pension funds.

The death benefits as well as any spouse’s or orphan’s pensions will be paid as soon as the necessary documents, such as the list of heirs, birth certificate or confirmation of full-time education, have been submitted.

Departure / change of employment

Where members leave Hitachi Energy, the pension funds will pay the corresponding vested benefits to the new employer’s pension fund or to a vested benefits institution (lock-up account) if there is no new employer.

Vested benefits are paid directly to departing members if they leave Switzerland (or the Principality of Liechtenstein)* or take up self-employment.

If the company terminates the employment relationship, members may voluntarily continue their pension insurance with the Pension Fund provided they are at least 55 years of age and are not insured with another pension fund through a new employer. This means that the pension cover remains in place in the event of unemployment and a retirement pension can be drawn at a later date. Where such members join a new company and are admitted to a new pension fund, they will leave the Hitachi Group Pension Fund as a matter of principle.

At the start of their continued insurance, members choose whether they wish to pay the savings contributions in addition to the risk contributions. The savings capital will continue to accrue in the Pension Fund and will earn interest.

Further information is available in the Continued Insurance leaflet.

* This does not apply to the mandatory portion of the termination benefits, provided that the departing member settles in an EU country and is subject to statutory insurance against old age, disability and death in that country. In this case, the mandatory portion must be used to set up a vested benefits account or a vested benefits policy in Switzerland or the Principality of Liechtenstein.

Disability

Members who are at least 40% disabled as defined by the Swiss Federal Disability Insurance (IV) are entitled to a disability pension. Members must be insured with the Pension Fund at the onset of the incapacity for work whose cause led to their disability. As a rule, the Pension Fund pays the PF disability pension after expiry of the sickness daily allowance.

Divorce

In the event of a divorce, the court automatically sends the divorce decree to the Pension Fund and notifies the Fund of the vested benefits to which the former spouse is entitled. The Pension Fund then transfers this amount to the spouse’s pension fund or to a vested benefits account.

Marriage

All marriages must be reported to the HR office which will pass on the information to the Pension Fund. The Pension Fund will then calculate the vested benefits at the time of the marriage and report this value on the insurance certificate.

Partners

If unmarried members have lived verifiably in the same household with an unmarried, unrelated domestic partner for an uninterrupted period of at least five years prior to the member’s death, or if they were responsible for the maintenance of one or more joint children, the deceased member’s partner is entitled to the same benefits as a spouse, provided that a respective application is submitted no later than three months after the death of the member.

Residential property

Members may invest their savings capital in home ownership up to three years before reaching the retirement age set out in the Rules. The minimum withdrawal is CHF 20,000.

Up to the age of 50, members may withdraw their entire savings capital; after this age, they may withdraw the amount of their savings capital at the age of 50 or half of the current accrued savings capital.

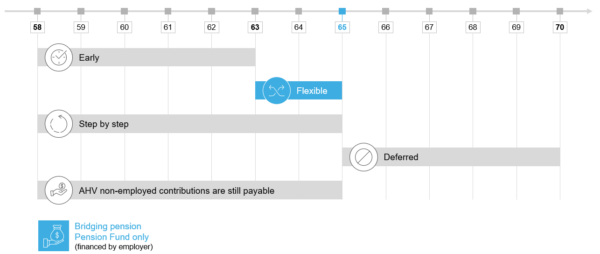

Retirement

At their own request, members may retire at the earliest at the age of 58. The notice period is two months. With the company’s consent, members may postpone their retirement at the latest until the age of 70.

The savings capital is equal to the capital accrued at the time of retirement. Retirement benefits from the Pension Fund may be drawn in the form of lump-sum capital and/or as a retirement pension. If the entire capital is withdrawn, all claims against the Pension Fund are settled. Members have the option of drawing only a portion of the savings capital as a lump-sum upon retirement. In this case, the retirement pension and other insured benefits (e.g. spouse’s/partner’s and orphan’s pension) will be adjusted accordingly.

It is also possible to reduce the retirement pension in favour of a higher spouse’s or partner’s pension at a later date.

In the Supplementary Insurance Plan, retirement benefits are exclusively provided as lump-sum capital.

Date of retirement

Flexible retirement

In the event of retirement after the 63rd birthday, the retirement pension is calculated on the basis of the savings capital accrued at the time of retirement and the conversion rate. From the time of retirement until the statutory retirement age (age 65), members liable to pay contributions are up to 2028 entitled to a monthly bridging pension, provided that they have paid contributions for at least five years. The bridging pension is equal to the maximum AHV retirement pension applicable at the time of retirement. For part-time employees, the bridging pension is reduced on the basis of the average level of part-time work during the last five years. The bridging pension is financed by the employer.

Early and deferred retirement

As a rule, members whose employment is terminated at the age of 58 will take early retirement. However, under certain conditions, they may request the transfer of the termination benefits or, if the employment relationship was terminated by the company, the continuation of their pension insurance with the Pension Fund. With the consent of the company and pursuant to Art. 33b BVG, members may postpone their retirement until they reach the age of 70 at the latest. The Pension Fund calculates early or deferred retirement pensions on the basis of the savings capital accrued at the time of retirement and the conversion rate.

Phased retirement (partial retirement)

With the company’s consent, members may opt for partial retirement and retire in stages. This requires a reduction in the level of employment. At present, the retirement pension can be drawn in up to three stages. Depending on the tax authority of the canton, different regulations apply to the minimum number of stages and the option of lump-sum withdrawals. In terms of tax law, a stage comprises all lump-sum withdrawals within a calendar year. We advise members to obtain the relevant information from the tax authorities.