Good to know

Employee benefits made easy

Click here to find out all you need to know about the Hitachi Group Pension.

Avadis Vermögensbildung SICAV

As a means of promoting private pension insurance, Avadis Asset Growth offers employees resident in Switzerland the opportunity to invest their assets with the Avadis Asset Growth foundation at favourable conditions.

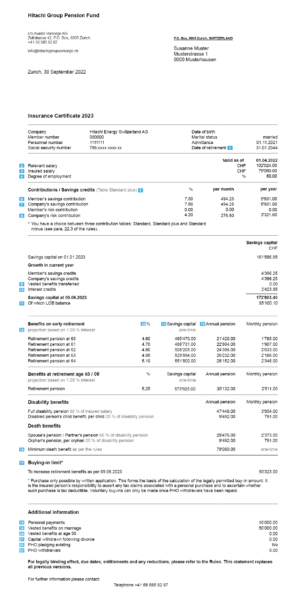

Insurance certificate made easy

1 | The last day of the month in which a member turns 65 is referred to as the date of retirement.

2 | As a rule, the relevant annual salary is 13 times the monthly salary.

3 | The insured salary is the relevant salary less the coordination deduction. For members in part-time employment, the maximum coordination deduction is weighted according to the employment level.

4 | Employment level agreed with the employer in the employment contract

5 | Selected countribution table

6 | The savings contributions payable by the member and the company are charged as of 1 January of the year in which the member reaches the age of 25. They are deducted from the member’s salary as a percentage of the insured annual salary and credited to the retirement account, depending on the selected contributions table and the member’s age.

7 | The savings contributions payable by the member and the company are charged as of 1 January of the year in which the member reaches the age of 25. They will be deducted from the salary as a percentage of the insured annual salary in accordance with the Standard contributions table and the member’s age and will be credited to the retirement account.

8 | At the Hitachi Group Pension Fund, the risk contribution that finances the risks of death and disability is paid in full by the employer from age 25 onwards.

9 | When new employees join the company, the savings capital they have accrued at their former pension fund (vested benefits) will be transferred to the new pension fund of the new employer. To this end, the employees have to give the former pension fund the transfer details of their new pension fund.

10 | Interest on savings capital since the beginning of the year: the interest rate is set by the Board of Trustees. In this example, the interest rate is 1.5%.

11 | Minimum benefits as per BVG – The Law on Occupational Retirement, Survivors’ and Disability Pension Plans (BVG) requires all registered pension funds to maintain accounts in accordance with BVG standards (so-called shadow accounts). The shadow account specifies the minimum statutory BVG benefits that the pension fund must guarantee.

12 | Interest rate used to extrapolate the benefits. This rate may differ from the effective interest rate.

13 | The conversion rate is used to calculate the expected annual pension on the basis of the projected savings capital.

14 | The projected savings capital represents the pension assets expected to have been accrued at retirement age. The projected savings capital takes into account the current savings capital as well as the future employee and employer savings contributions including interest.

15 | The projected annual pension is calculated as the projected savings capital multiplied by the conversion rate.

16 | In the event of death before retirement, the amount of the death benefit is equal to the accrued net savings capital (savings capital less personal buy-ins into the Pension Fund), less the costs of financing the survivors’ benefits; however, at least 100% of the insured salary.

After retirement, at the latest after the statutory retirement age, the death benefit is equal to twice the annual retirement pension, reduced by the retirement pensions already drawn.

17 | In accordance with the legal provisions, contributions may be paid into the Pension Fund at any time in order to increase the retirement benefits. The Pension Fund determines the buy-in limit pursuant to recognised principles, see Rules.

18 | Buy-ins

19 | By law, the vested benefit is calculated and recorded at the time of marriage or the registration of a partnership. In the event of a divorce or dissolution of a partnership by the courts, this figure serves as a reference value for the calculation of the distributable termination benefit.

20 | Members who have passed the age of 50 may withdraw no more than the vested benefits to which they would have been entitled at the age of 50, or half of the vested benefits at the time of withdrawal.

21 | In the event of a divorce or dissolution of a registered partnership, a vested benefit must be transferred to the ex-partner if he/she is eligible for compensation. However, the law entitles members to make voluntary contributions / buy-ins into the Pension Fund at any time up to the amount of the transfer.

22 | Members have the option of pledging all or part of their vested benefit entitlement to buy their own home.

23 | Members can use their savings capital to buy their own home. This is possible up to three years before reaching the retirement age specified in the Rules. The minimum withdrawal is CHF 20,000. Up to the age of 50, the entire savings capital can be withdrawn; after the age of 50, the amount of the savings capital accrued at the age of 50, or half of the current accrued savings capital, can be withdrawn.

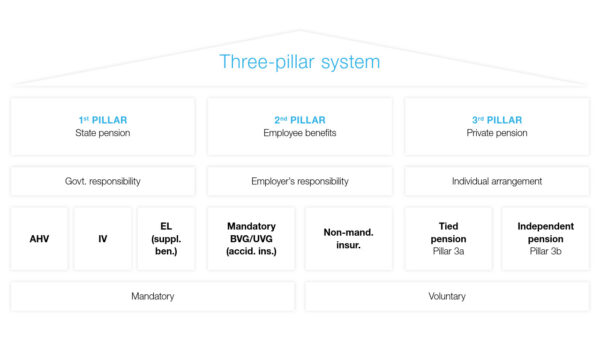

The Swiss pension system

The Swiss pension system is based on three pillars: state pension insurance (1st pillar), pension funds (2nd pillar) and private pension insurance (3rd pillar). The three pillars replace income from employment and provide financial security in the event of old age, disability and death. The 1st and 2nd pillars are mandatory and the respective contributions are automatically deducted from the salary. The 3rd pillar is optional.

Switzerland’s three-pillar system: